Understanding how to interpret a credit card statement is a fundamental aspect of financial literacy, but it may appear overwhelming, especially for first-time credit card users or those who have recently changed banks. To add to this complexity, different financial institutions have various ways of displaying the rewards earned from points or cash back during the preceding billing cycle.

By mastering the art of reading your credit card statement, you’re poised to make more informed financial choices. This knowledge allows you to track your spending, monitor your credit usage, and see the rewards you’ve accrued. Here’s a guide on how to interpret your credit card statement.

What exactly is a credit card statement?

A credit card statement is a document, either physical or digital, that outlines all transactions charged or refunded to your account during a specified billing cycle. This statement encompasses purchases, pre-authorizations, annual fees, and refunds.

Typically, billing cycles last for one month, and cardholders are granted at least 21 interest-free days. Provided you pay your entire balance punctually by the due date, no interest charges will apply.

Each credit card statement contains several key pieces of information:

- Credit card –At the top of the statement, you’ll find the name of the credit card along with your personal name. This is crucial if you own multiple credit cards from the same issuer.

- Your name and credit card number –Below the card name, the statement will list your name and credit card number, though some digits may be obscured for security reasons.

- Statement date –This date indicates when your statement was generated.

- Statement period –This signifies the range of dates during which transactions were captured.

- Transactions –This section details several items, including the transaction date (when the purchase occurred), the post date (when the charge was formally added), the activity description (usually the merchant’s name), and the amount charged.

- Total new balance –This indicates the current amount you owe. A negative figure suggests you have a credit balance.

- Contact information –Phone numbers for your bank and loyalty program (if available) will be displayed here.

- Points/cash back earned –If you have a rewards credit card, this section summarizes the rewards accrued during the billing cycle.

- Payment information –This crucial part of your statement shows the due date for payments, your credit limit, available credit, and your annual percentage rate (APR) for purchases and cash advances.

- Estimated time to pay –This estimate reflects how long it would take to pay off your total balance if you only made the minimum payments each month.

- Calculating your balance –This section may list any fees incurred during the month, such as those from balance transfers, cash advances, interest, and late payments.

- Payment details –At the end of your statement, a tear-off portion outlines payment details for those who prefer to pay by mail or at a physical location.

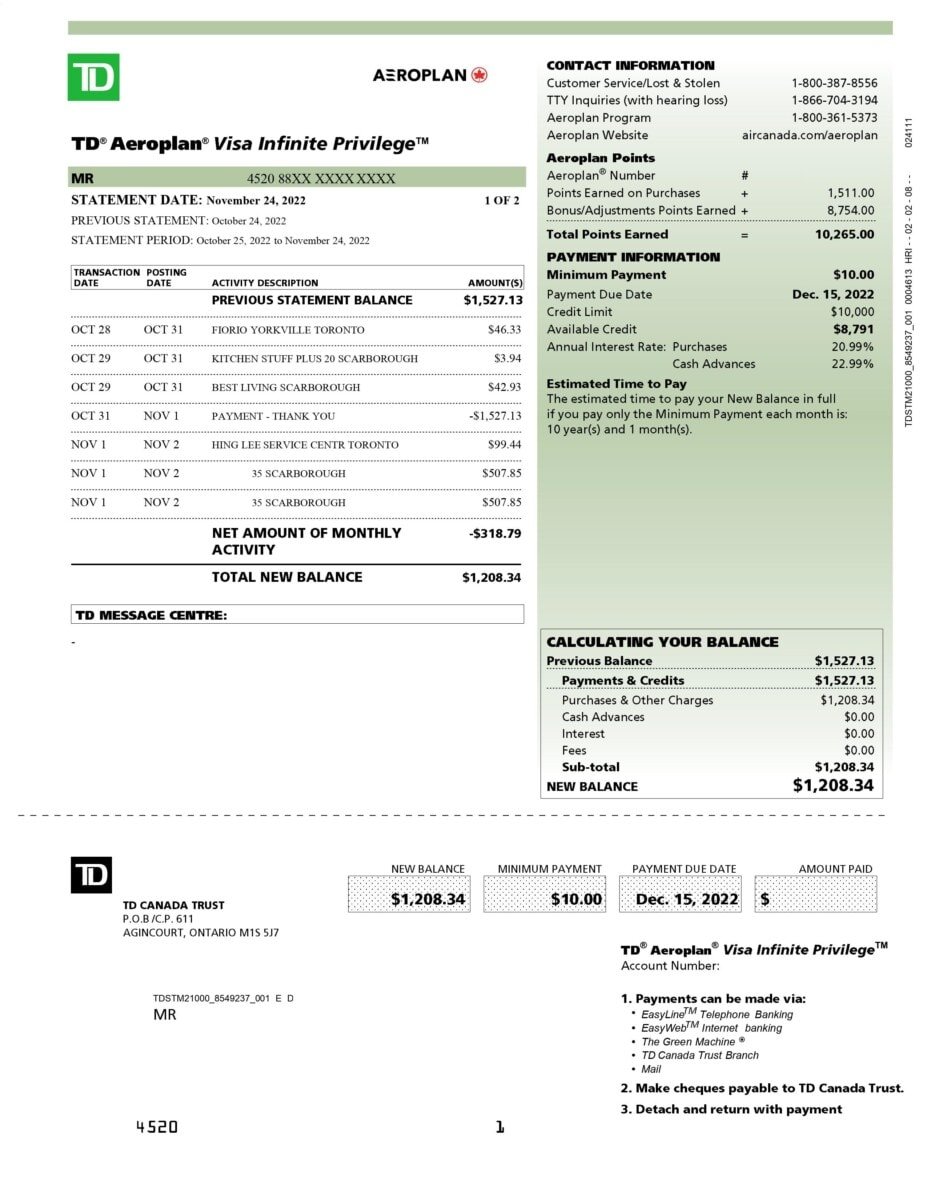

Sample credit card statement

To enhance your understanding of how to read a credit card statement, consider this example.

This statement is from my TD Aeroplan Visa Infinite Privilege Card. I always focus on the transactions and the Aeroplan points accrued.

Frequency of credit card statements

You might wonder how often credit card statements are issued. Generally, they are generated monthly right after the billing cycle concludes. If you choose paperless statements, they will be accessible through your online banking portal, and you will receive an email notification once your statement is ready. For those opting for physical copies, statements will arrive in your mailbox a few days following the statement date.

While paper statements can be convenient, some credit card issuers may provide incentives for switching to paperless options, such as bonus points or cash back offers.

Your statement date typically corresponds to the day you initially opened your credit card account. For instance, if you enrolled on the 17th, the statement date will usually occur on the 17th of each month. You can request a change in your statement date by contacting your credit card provider.

Things to check on your credit card statement

When learning how to read a credit card statement, there are certain aspects you should review each month:

- Suspicious transactions –Thoroughly examine the transactions section for any purchases that seem unfamiliar. If you locate any charges you did not authorize, research the merchant. Should you confirm that an unauthorized charge was made, contact your financial institution to initiate a fraud investigation.

- Interest and fees –For those who consistently pay their bills fully and on time, checking for interest and fees listed under the balance calculation section is essential to ensure no unexpected charges, like balance protection fees, were applied.

- Credit card balance –It is crucial to be aware of your current balance, as that reflects how much you owe and informs your payment decisions.

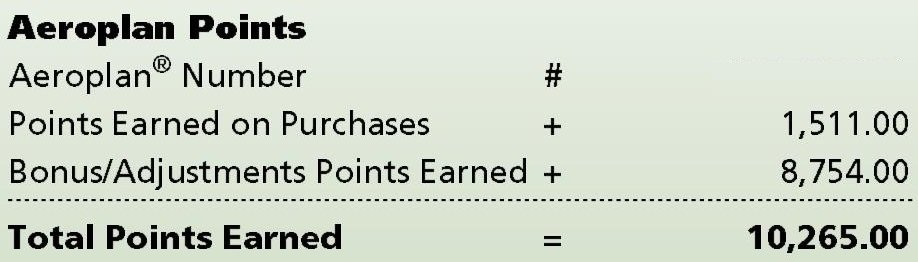

Understanding points and cash back calculations on credit card statements

If you earn points or cash back through your credit card, scrutinizing the details of your rewards program is important. For cash back credit cards, the computation is fairly straightforward, based on the earn rate associated with your card.

In contrast, points cards may involve a more intricate breakdown of how rewards are calculated. Referring again to the TD Aeroplan Visa Infinite Privilege credit card statement, keep in mind that each rewards program has its own specifics.

In this depiction, you can see points accrued from purchases alongside bonus or adjustment points. While it should be a simple matter, TD/Aeroplan tends to complicate the explanation. Points earned reflect the standard earning rate of 1.25 Aeroplan points for each dollar spent. For eligible purchases like gas, groceries, travel, and dining, the earning increases to 1.5 points per dollar. The additional 0.25 points appear under bonus/adjustment points earned. Any promotional bonus points also fall into this category. For the referenced statement, I earned an extra 5,000 Aeroplan points for spending $1,000.